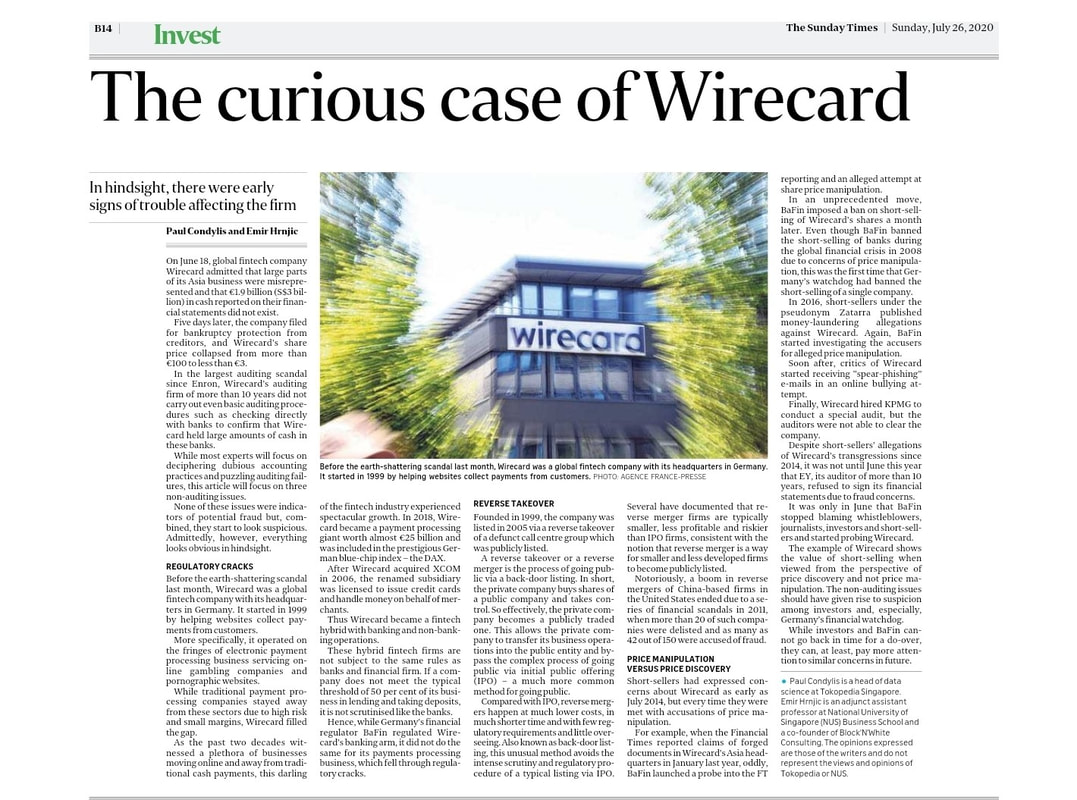

|

Washington Post:

Murky past of China’s Focus Media provides lesson By — Pedro Matos, Emir Hrnjic and Lianting Tu July 17, 2015 The big idea: The extreme volatility in the Chinese stock market is challenging foreign investors. China has emerged as the world’s second-largest economy, but does this momentum translate into investment opportunities? The scenario: One such opportunity might be the Chinese media market, which has a potential audience of more than 1.3 billion people. But government restrictions on direct foreign ownership and on content mean that investors must invest in Chinese-based companies. In 2005, Focus Media Holding was the leading digital media network in China. When it went public that year, it was the largest initial public offering of a Chinese company on the Nasdaq composite index. The number of China-based firms on U.S. stock exchanges peaked in 2010; at that time, Chinese firms represented more than 25 percent of all IPOs. In 2011, Muddy Waters, a U.S. short-seller fund and equity research firm, accused Focus Media of overstating the size of its business and deliberately overpaying for acquisitions. Muddy Waters had been involved in uncovering some of the most high-profile cases of fraud allegations in China. Four of the first five firms it targeted had to delist. Muddy Waters was named after the Chinese proverb “muddy waters make it easy to catch fish,” which suggests that nontransparent markets allow for opportunistic behaviors. The resolution: Focus Media’s stock price fell sharply at first but rebounded as the company countered Muddy Water’s attacks. In 2012, the SEC launched an investigation and pressured Focus Media to amend some of its filings. Focus Media was taken private in a deal valued at more than $3.7 billion — China’s largest-ever buyout. In the following months, several Chinese companies followed suit and delisted from the Nasdaq. As of 2015, private-equity investors in Focus Media are looking to exit from the deal. Going public in Hong Kong appears to be the preferred option, but the situation remains murky. The lesson: Cases such as Focus Media, and the challenges and opportunities surrounding Alibaba’s high-profile IPO in 2014, illustrate how attention to corporate governance and an understanding of regulatory differences will continue to be a priority for investors in the Chinese market. Investors should keep several ideas in mind: ●Don’t make the assumption that financial statements and filings can’t be changed; in some cases, fraudulent practices, in any country, do not become obvious for some time. ●Be careful about basing an investment decision purely on the favorable-looking economic or GDP-based growth characteristics of a country or region. ●Understand governmental and regulatory restrictions on ownership as part of your research and be sure to understand exactly what you’re investing in. In other words, make sure the water is clear. — Pedro Matos, Emir Hrnjic and Lianting Tu Matos is an associate professor at the University of Virginia Darden School of Business. Emir Hrnjic and Lianting Tu are with National University of Singapore.

0 Comments

ThinkBusiness.nus.edu.sg

Alibaba’s New York IPO: A wake-up call for Asia By: Dr Emir HRNJIC September 8, 2014 Over the past two decades, we’ve become used to hyperbole about the latest “big thing” to come roaring out of the thundering engine that is the Chinese economy. In the case of e-commerce giant Alibaba, however, we have an example that is living up to the hype. When Alibaba floats on the New York Stock Exchange, it is expected to be one of the biggest IPOs in history – a watershed moment for Chinese firms, especially Chinese tech firms, on the global stage. Most analysts expect the IPO to eclipse Facebook’s $16bn floatation in 2012 and possibly even the 2008 Visa IPO, the largest ever in the US. But the decision to float in the US also marks something of a wake-up call for exchanges here in Asia, who risk losing out on some high value listings unless they prove more accommodating to firms pushing for dual class offerings. Once Alibaba stocks start trading – now expected sometime in September – speculation is high that the firm will raise $20bn or more. That would value Alibaba at around $150bn, an amazing feat for a business founded in 1999 by English teacher Jack Ma. Ma had originally wanted to list Alibaba in Hong Kong and spent more than a year trying to do so. The territory seems a natural fit because of language as well as cultural and geographical proximity. In addition, the overwhelming bulk of Alibaba’s revenues - 86.9 per cent in 2013 - originate within greater China and investors there, many of whom have used Alibaba’s services, understand its business. Nevertheless, Hong Kong regulators rejected Alibaba’s application due to its unique (and complex) governance structure, designed to keep control within a small group of partners. In process, regulators overlooked the provision which allows dual-class share structure under “exceptional circumstances” (Rule listing 8.11); perhaps to avoid setting a potentially awkward precedent. Either way, after a year of talks, the inflexibility of Hong Kong regulators prompted Alibaba to turn its attention instead to the US market. The move marked a significant loss for Hong Kong, which missed out on a prestige opportunity to add a dynamic and high-profile tech firm to its listings and diversify its China listings away from the current concentration on the finance and property sector But Alibaba’s decision to list in the US also has important implications for Asian regional markets as a whole, including here in Singapore which has seen a dearth of major IPOs in recent months. Singapore also expressly bans dual-class shares because of concerns over “entrenchment of control”. The only exception to this rule is media group Singapore Press Holding; its “management” shares have 200 votes each as compared to “ordinary” shares with one vote each. The pervasive criticism of dual class structures in Asia is that they are unfair, giving one group of shareholders disproportionate influence over corporate governance. Specifically, dual class share structures give this one (usually very small) class of shareholders higher voting rights than another class, although both are entitled to the same dividends. For instance, a firm’s founder may hold 5 per cent of cash flow rights, while holding 50 per cent of voting rights. Alibaba, for its part, wants to retain a corporate partnership structure that gives the firm’s founding partners effective control of the board. The reasoning, it says, is to preserve the firm’s culture shaped by the founders. It’s a similar model to that found in other major internet floatations such as LinkedIn, Facebook and Google. In fact, dual-class share structures have been allowed on all United States exchanges since 1985, and have been used by more than six hundred firms, including Nike, Visa, and Manchester United. Costs and benefits But critics of dual-class share structures argue that they are not equally fair to all shareholders and could even be detrimental to the interests of those with lower voting rights. Shareholders with higher voting power, usually top executives, may decide to consume extravagant perks and take excessive risks, with the consequences disproportionately borne by other shareholders who have almost no say in the matter. Studies have found that companies that have insider voting rights, such as in a dual-class share structure, also tend to have lower market value. This suggests that a company’s founder may decide to accept a lower valuation of the company in order to maintain control. One recent study also found that CEOs of companies with dual-class share structures receive higher compensation and make worse acquisitions. But such structures clearly have benefits too. Proponents argue that they allow controlling shareholders to pursue their long-term vision, protecting the firm from pressure from public investors who prefer short-term outcomes. Dual class listings can also incentivise and ease the transition for company founders to take their companies public, without the fear of losing control. Moreover, compared to other ways of retaining founder control - such as pyramid ownership or cross-shareholdings like those frequently used in countries such as South Korea and Japan – the dual-class share structure is simpler and more transparent. Another stream of research shows that shareholder value is improved by dual-class share recapitalisations, which is when companies with a single-class share structure adopt a dual-class share structure. Compared to single-class firms of similar sizes within the same industry, such firms have grown on average 20 per cent more than other firms and earn 23.11 per cent higher stock returns over a four-year period. Two factors have been shown as critical in determining whether firms and their shareholders benefit from having a dual-class share structure: the transparency of the company, and the level of its managers’ talent. On the former, recent empirical studies have shown that transparent dual-class share structure firms perform better. For example, a decrease in opacity of 10 per cent for a founder-controlled firm with a dual-class share structure led to a 5.2 per cent increase in firm value, compared to non-dual-class, non-founder controlled firm of a similar size and in the same industry. This is consistent with the notion that insiders in transparent firms focus on shareholder value enhancement, while those in opaque firms are more likely to seek to entrench themselves. The recent theoretical model suggests that dual-class firms with talented managers perform better, while those with less talented incumbents may use the dual-class structure to exploit minority shareholders and destroy the value. Implications for SGX The question then is if the US has managed to successfully implement dual-class share listings - and in doing so lured major IPOs like Alibaba away from Asia - is it time to for markets here in the region, such as Singapore’s SGX, to follow suit? One caveat is that circumstances in the US are different from those in Asia. The exchanges there are more mature and there are more influential and activist investors. In addition, the US has a strong litigious culture, where minority shareholders can sue a company if the controlling shareholders abuse their power or breach their fiduciary duty. Such a culture is far less entrenched here in Asia. Having said that, in the light of Alibaba, it may be time for the SGX and others to look at whether dual-class share structures are now workable here, to attract successful companies whose founders are reluctant to cede control. In Asia, with its plethora of family firms, it is conceivable that many need capital but are concerned with potentially losing control of their companies. At the same time, investors' concerns over potential corporate abuse could be alleviated through a simultaneous improvement of regulatory enforcement, transparency and corporate governance. Even though controlling shareholders have the power to elect directors to the board, the directors still have a duty to safeguard the interests of all shareholders. Hence, a possible governance safeguard would be to mandate a greater number of independent directors and give them control of the nominating committee, thereby ensuring strong oversight and monitoring of top management. Another measure might be to impose extra disclosure requirements on dual-class IPOs – such as higher disclosure standards for related party transactions and executive compensation – to minimise the chance of corrupt activity. As oversight and corporate governance are enhanced, investors' concerns over dual-class listings will be alleviated. After all, the objectives of improving regulatory enforcement, transparency and corporate governance are already a priority for our regulators. Above all Alibaba’s decision to list in the US has shown that markets here in Asia need, at the least, to reconsider their approach or risk losing out on major IPOs. SIDE BOX: Alibaba: The rise of an e-commerce ecosystem Alibaba was founded in 1999 by Jack Ma out of his apartment in the Chinese city of Hangzhou. Today Ma, who revels in his self-created rock star personality, is chairman of one of the planet’s biggest e-commerce firms, with a growing portfolio of services bringing in an annual turnover dwarfing that of Amazon and eBay combined. Ma has summed up his vision for Alibaba saying he does not want to build the company into an empire, but rather into an “ecosystem”. “Every empire will be toppled someday, but an ecosystem is sustainable,” he told reporters last year. For Alibaba to build its own ecosystem – funding a spate of acquisitions and development of new services - it needs cash. Hence the decision in 2013 to go for an IPO. The Straits Times

Singapore Should Sharpen Its Edge in Islamic Finance By: Dr Emir Hrnjic July 22, 2014 AT the 2014 World Islamic Banking Conference in Singapore last month, Mr Ravi Menon, managing director of the Monetary Authority of Singapore (MAS), asserted that “the sun is shining on Islamic finance”. Indeed, over the past decades, the global Islamic finance industry – which refers to financial activities compliant with Syariah law – has grown faster than other financial sectors, mostly thanks to petrodollars, changing demographics and the establishment of the Islamic Development Bank. Global Islamic banking assets surpassed S$2.25 trillion in 2013, while Standard & Poor's and the Ernst and Young World Islamic Banking Competitiveness Report have projected that the industry would be worth between S$2.5 and S$3.75 trillion by 2015. Putting it in context, another finance industry that has experienced dramatic growth recently - hedge funds - managed S$2.5 trillion worth of assets in 2013. To be sure, Singapore has not stayed on the sidelines. To encourage the sector’s growth, MAS has levelled the regulatory playing field for Islamic and conventional finance, and introduced tax incentives for Islamic finance in 2008. The city-state also recorded several milestones such as Sabana's listing of the world's largest Islamic Reit, Khazanah Nasional's issuance of S$1.5 billion worth of Islamic bonds, and Parkway Holdings' S$750 million Islamic syndicated loan. However, Singapore was a late entrant into this industry; MAS only joined the Islamic Financial Services Board in 2005. Globally, the Islamic finance industry in Singapore, with assets of roughly S$11 billion, lags far behind that of Saudi Arabia (estimated S$258.7 billion of Islamic assets), Malaysia (S$132.5 billion), and UAE (S$93.75 billion). According to the Islamic Finance Country Index, Singapore is ranked 23rd in the world, behind countries such as Britain. Singapore issuers have launched more than S$4 billion of Islamic bonds to date – a mere 4 per cent of the S$105 billion issued by neighbouring Malaysia last year alone. Some benefits of Islamic finance THERE is good reason to worry about Singapore missing out on this fast-growing area of finance, which brings benefits not just to the overall economy but to individual issuers and investors as well. My colleague Professor David Reeb, the Government of Dubai's Mr Harun Kapetanovic and I recently analysed Emirates Airline's US$1 billion (S$1.25 billion) Islamic bond issue last year, during which the firm also issued US$750 million (S$937.5 million) via conventional bonds. Even though the airline’s conventional bonds had similar maturity and appeared to have similar risk, the Islamic bonds provided capital at a significantly lower cost – a difference of roughly 50 basis points or S$6.25 million in interest cost savings per year. This most likely arose from the huge mismatch between demand and supply for Islamic finance products. For every Islamic bond issued, there are, at least, two willing buyers. Similar benefits have been seen by other companies that issued Islamic bonds, vis-à-vis those that issued conventional bonds. Firms that raise capital through Islamic bonds do so at a lower cost, while Islamic bonds provide an opportunity for Islamic institutions to invest in Syariah-compliant securities issued by reputable companies with strong credit credentials. Competition heating up AT the same time, other international financial centres – including those without a Muslim population as large as Singapore’s – have jumped on the bandwagon. Britain successfully issued a 200 million pound (S$425.7 million) Islamic bond in June 2014, making it the first Western country to sell such bonds. This amount may seem like a tiny fraction of the overall Islamic bonds market, but the issue was 10 times oversubscribed and underpins London's efforts to be a global hub for Islamic finance. Luxembourg, another large European financial centre, is now preparing to sell €200 million (S$337.8 million) worth of sovereign Islamic bonds. In the Middle East, the Islamic finance industry centred in Dubai includes commercial banking, asset management, Syariah consulting, insurance, endowments, and other financial services. Islamic assets in Dubai have grown 15 per cent yearly and represented about 16.7 per cent of overall finance in the emirate last year. Closer to home, Hong Kong has shrewdly and aggressively started developing Islamic finance by intensifying its ties with Malaysia, another credible hub. The government is working on issuing its first sovereign Islamic bond, potentially worth U$500 million (S$625.15 million which would mark a milestone for the Asian market. Cementing Singapore's role AGAINST this backdrop, Singapore can, and should, foster further growth of Islamic finance domestically so that the country does not get left behind. Singapore can find its own niche in Islamic finance by relying on its key strengths. While Malaysia has become the leading hub for Islamic bond issuance, with a market share of more than half of the global Islamic bonds outstanding, Singapore can focus on Islamic wealth management, for instance. Islamic wealth management is based on long-term relationships and investor confidence; Singapore’s well-known reputation for safety, security and stability will provide a distinct advantage in the global market. The city-state could promote itself as a preferred destination for high-net-worth individuals in search of world-class Syariah-compliant wealth management services and products. Like Hong Kong, Singapore should also leverage on Malaysia's organic Islamic finance strengths, while Malaysia (and Indonesia, another Muslim-majority nation) at the same time could benefit from Singapore's strength as an international wealth and financial management centre. In addition, with the strong and growing international demand for Islamic financial products, Singapore could potentially become a global intermediary between institutional investors and firms in need of funds. With the help of the Singapore Exchange, it could become a major trading arena for Islamic bonds, hence increasing liquidity in these bonds in the process. To that end, Singapore should consider issuing government Islamic bonds regularly, preferably with differing maturities, to attract international Islamic capital, while providing a benchmark for potential corporate issuers. Given that Islamic bonds are sometimes issued at the same yield as conventional bonds’, the sovereign version could even appeal to non-Islamic investors, such as the Central Provident Fund. Once there is enough critical mass here, it could be advantageous to provide a benchmark for Islamic equity investments, which can be achieved through either a Singapore Islamic Exchange Traded Fund, similar to iShares MSCI USA Islamic, or a Singapore Islamic index, similar to the Dow Jones Islamic Market Index. The government would need to establish clear rules for the industry, possibly through the introduction of a central Syariah Board to provide clear guidelines, similar to MAS' banking codes. In addition, Singapore needs to strengthen the connections between academia, business, and government to develop the necessary human capital and financial technology that supports a comprehensive and holistic Islamic finance ecosystem. To that end, the government could consider building an institute for education and research in Islamic finance to develop the necessary human capital, educate future industry leaders, and advance knowledge in this area. This new initiative should preferably be hosted by a Singapore university, while leveraging the academic strengths of all tertiary institutions in Singapore, including those headquartered overseas. Similarly, MAS, in collaboration with the institute, could jointly help to attract top scholars in the field to share their knowledge as well as to showcase academic expertise based in Singapore. This could be achieved by organising more high quality international conferences. Finally, MAS had introduced an initiative to provide tax incentives for Islamic finance in 2008, which had a fixed five-year tenure, but these incentives recently expired. Potential future tax incentives should preferably include tax deductions on the cost of issuance, exemption from income tax for Special Purpose Vehicles (SPV), and tax deductions for the SPV originator company. In conclusion, Islamic finance in Singapore has yet to reach its full potential. Success in this sector needs robust, long-term government support. The game is global, and only long-term players will prosper. Dr Emir Hrnjić is director of education and outreach at the NUS Business School's Centre for Asset Management Research and Investments. The Business Times, June 4, 2014

Where Dual-Class Structure Might Work By Dr. Emir Hrnjic THE Singapore Exchange (SGX) has been in the news lately, but not for the right reasons: commentators have noted the relative dearth of major initial public offerings (IPOs) on the local bourse in recent months. To its credit, the SGX has tried to spice things up, most recently by proposing to make it easier for foreign companies already listed elsewhere to have a secondary listing in Singapore. But one other way it could help revive the moribund IPO market is to reconsider introducing dual-class listing structures. Such structures have generated controversy over the years, as they allow differentiation among a company’s shareholders, which is considered by some to be unfair. They give one class of shareholders higher voting rights than another class, even though both classes are entitled to the same dividends. Dual-class share structures have been allowed on all United States exchanges since 1985, and have been used by more than six hundred US firms, including Nike, Visa, Google and Facebook. But they are not as welcome in Asia. They have been expressly banned on the SGX, because there are concerns about the “entrenchment of control”. The only exception to this rule is Singapore Press Holding; its “management” shares have 200 votes each as compared to “ordinary” shares with one vote each. Hong Kong’s stock exchange (HKEx) technically allows such structures in “exceptional circumstances”, although this provision has never been exercised. As a result, regional bourses have sometimes lost out on plum listings. Earlier this year, in what is set to be one of the largest IPOs in history, China’s Alibaba Group shunned the HKEx and instead opted to list in New York – partly because of the HKEx’s reluctance to let Alibaba get around its ban (?) on dual-class shares. Costs and benefits Critics of dual-class share structures argue that they are not equally fair to all shareholders. Shareholders with higher voting power, usually top executives, may decide to consume extravagant perks and take excessive risks, with the consequences disproportionately borne by other shareholders who have almost no say in the matter. Companies that have insider voting rights, such as in a dual-class share structure, also tend to have lower market value according to studies by Gompers, Ishii and Metrick in Review of Financial Studies (2010) and Smart and Zutter in Journal of Financial Economics (2003). This suggests that a company’s founder may decide to accept a lower valuation of the company in order to maintain control. A recent study by Masulis, Wang and Xie in The Journal of Finance (2009) have also found that CEOs of companies with dual-class share structures receive higher compensation and make worse acquisitions. But such structures clearly have benefits too. Their proponents argue that they allow controlling shareholders to pursue their long-term vision, protecting them from public investors who prefer short-term outcomes. They also incentivise company founders to take their companies public without the fear of losing control. Moreover, compared to other ways of retaining founder control, such as pyramid ownership or cross-shareholdings – frequently used in some countries such as South Korea and Japan – the dual-class share structure is simpler and more transparent. Another stream of research shows that shareholder value is improved by dual-class share recapitalisations, which is when companies with a single-class share structure raise funds by adopting a dual-class share structure to issue more shares. Such firms grow 20 per cent more than other firms and earn 23.11 per cent higher stock returns over a four-year period, compared to single-class firms of similar sizes within the same industry. Whether firms and their shareholders benefit from having a dual-class share structure depends on two main factors: the transparency of the company, and the level of its managers’ talent. The recent empirical evidence by Anderson, Duru and Reeb in Journal of Financial Economics (2009) shows that transparent dual-class share structure firms perform better. A decrease in opacity of 10 per cent for a founder-controlled firm with a dual-class share structure leads to a 5.2 per cent increase in firm value, compared to non-dual-class, non-founder controlled firm of a similar size and in the same industry. Opacity index is constructed from trading volume, bid–ask spread, analyst following, and analyst forecast errors, while firm value is measured by Tobin’s Q which is calculated as the sum of the market value of equity, the book value of debt and the book value of preferred stock divided by total assets. This is consistent with the notion that insiders in transparent firms focus on shareholder value enhancement, while those in opaque firms are more likely to seek to entrench themselves. Theoretical model by Chemmanur and Jiao in Journal of Banking and Finance (2012) suggests that dual-class firms with talented managers also perform better, while untalented incumbents may use the structure to dissipate value. Anecdotal evidence The success of dual-class share structures can also be seen in some anecdotal cases. Warren Buffett’s Berkshire Hathaway, for instance, is one instance where founder control – albeit by a very talented founder – has resulted in handsome rewards for shareholders who don’t necessarily have the same voting rights. Berkshire Hathaway’s shareholders enjoyed a 19.7 per cent compounded annual return over the period 1965-2012, while the S&P 500 experienced a 9.4 per cent return in the period. In other words, a US$1,000 investment in Berkshire Hathaway in 1965 would have grown to a spectacular US$5.6 million in 2012, compared to a relatively modest US$74,600 for a similar investment in the S&P500. There are also situations where a company without a dual-class structure could have benefited from one. Apple's founding CEO Steve Jobs was forced out of the company he founded in 1985, leading to the decline of the company until his return in 1997. The series of initiatives he initiated in the following years helped make Apple the world's largest company. His original ousting could potentially have been prevented if, as the founder, he had owned “higher voting” shares – as other company founders like Facebook’s Mark Zuckerberg do. Implications for SGX If the US has managed to successfully implement dual-class share listings, should the SGX follow suit? One caveat is that circumstances in the US are different from those in Asia. The exchanges there are more mature and there are more influential and activist investors. In addition, the US has a strong litigious culture, where minority shareholders can sue a company if the controlling shareholders abuse their power or breach their fiduciary duty. Having said that, it may be time the SGX looks at whether dual-class share structures are now workable here, to attract successful companies whose founders are reluctant to cede control. In this region, with the plethora of family firms in South East Asia, it is conceivable that many need capital but are concerned with potentially losing control of their companies. Investors' concerns over potential corporate abuse could be alleviated through a simultaneous improvement of regulatory enforcement, transparency and corporate governance. Even though controlling shareholders have the power to elect directors to the board, the directors still have a duty to safeguard shareholders’ interest. Hence, a possible governance safeguard would be to mandate increased number of independent directors and give them control of the nominating committee, thereby ensuring strong oversight and monitoring of top management. Another suggestion would be to impose extra disclosure requirements on dual-class IPOs – such as higher disclosure standards for related party transactions and executive compensation – to minimise the chance of corrupt activity. As oversight and corporate governance are enhanced, investors' concerns over dual-class listings will be alleviated. After all, the objectives of improving regulatory enforcement, transparency and corporate governance are already a priority for our regulators. |

|